Securities finance in APAC: whitepaper

A closer look at the forces reshaping securities finance across APAC markets.

In Partnership with

APAC securities lending is evolving under the combined pressure of market structure, regulation, settlement change and digital innovation. This whitepaper examines the role of opportunity borrowing, the impact of T+1 on securities borrowing and lending workflows, and the growing influence of tokenised collateral across the region.

APAC lending revenues

Revenue

The market is defined by 85–90% opportunity-driven borrowing across more than 14 regulatory environments — making standardisation both valuable and complex.

Efficiency gains in this market would have a disproportionate impact on overall returns given revenue concentration.

Hong Kong momentum

Growth

Hong Kong combines strong lending revenues with a clear regulatory framework — its intent-based regime and designated securities list create a structured and attractive market.

The pace of growth reflects both underlying demand and the regulatory clarity that gives lenders confidence to participate actively.

Japan vs Australia

Structure

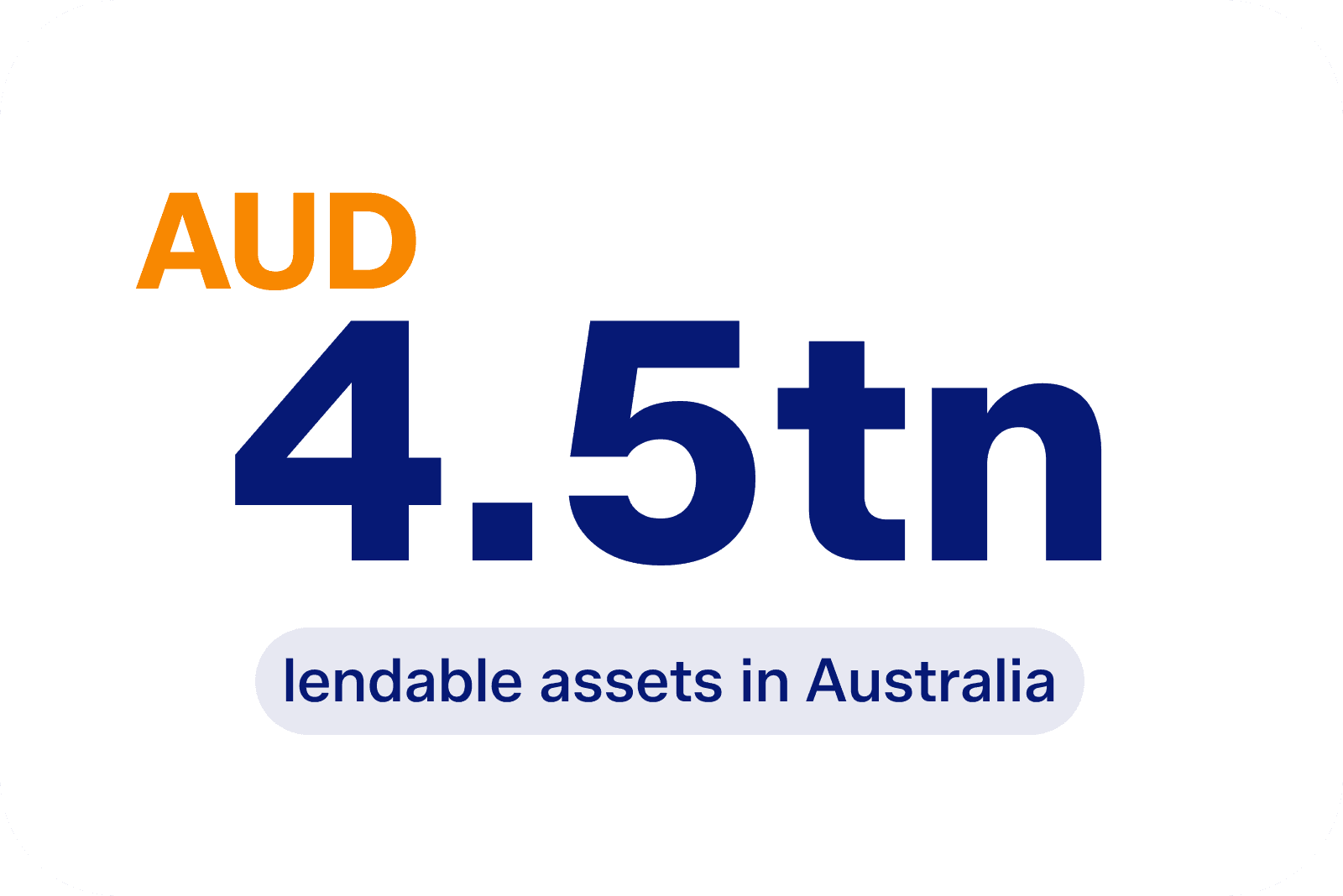

Japan is defined by a dual market structure and JGB collateral — Australia by tax rules and the scale of superannuation.

Understanding these structural differences is essential for firms looking to grow or optimise their APAC securities lending activity.

Securities finance in Asia-Pacific (APAC) is changing as regional market structures, settlement reform and digital infrastructure begin to reshape how liquidity is sourced and managed. The challenge for firms is not only navigating fragmentation, but understanding how borrowing models, operational design and collateral innovation will influence future competitiveness.

What is driving the next phase of securities borrowing and lending across APAC? How will T+1, market-specific structure and tokenised collateral affect regional workflows and liquidity formation?

The whitepaper examines the structural, regulatory and technological forces shaping securities finance in APAC. It looks at the dominance of opportunity borrowing, the implications of T+1 settlement cycles, the growing relevance of tokenised collateral and the distinct market dynamics emerging in Hong Kong, Japan and Australia.

The research, sponsored by FIS, highlights:

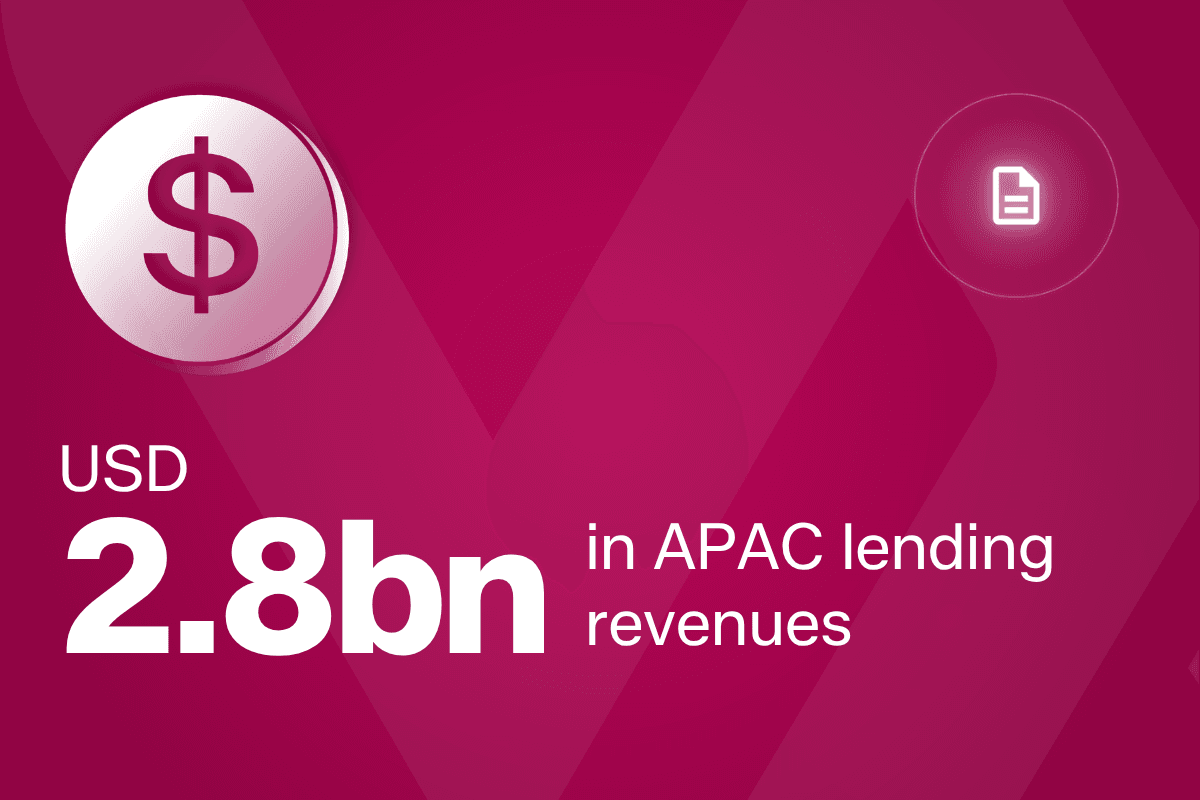

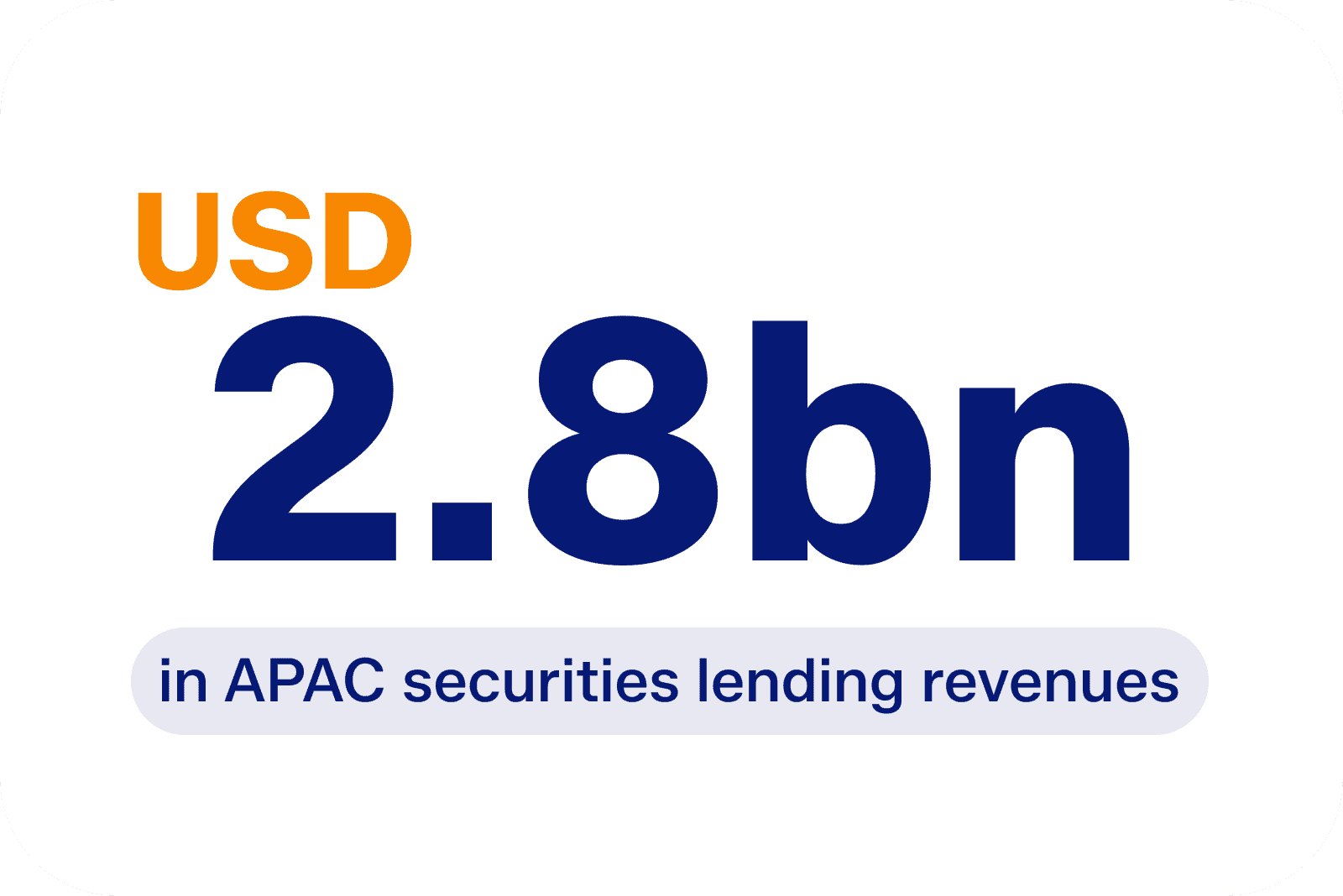

US dollar (USD) 2.8 billion in regional revenues: APAC securities lending continues to represent a significant commercial opportunity across diverse market structures

85–90% based on opportunity borrowing: most regional activity remains driven by opportunity borrowing rather than centralised programme models

T+1 reshaping securities borrowing and lending (SBL) workflows: shorter settlement cycles are expected to increase pressure on borrowing, inventory and operational timing across the region

Digital infrastructure is beginning to play a larger role in how firms think about collateral mobility and efficiency

Ask the Xchange AI

Have a question about our research? Ask our AI assistant for specific insights.

Authentication Required

You need to be logged in to access this content. Please sign in to continue.

You need to be logged in to access this content.

SHARE THIS INSIGHT